Vinokurov, E., Grichik, M., Tsukarev, T. (2022) New approaches to international reserves: the lack of credibility in reserve currencies. Russian Journal of Economics 8(4): 315-332. https://doi.org/10.32609/j.ruje.8.98242

This research paper aims to scrutinise all the solutions that can theoretically replace/supplement reserves in traditional reserve currencies. In addition, the authors look at the issue from the perspective of the Shanghai Cooperation Organisation (SCO) members and observers, as it is a leading platform where countries openly discuss this matter.

The freezing of Russia’s reserves was not the first case of such financial sanctions, but it contributed to the ongoing loss of confidence in traditional reserve currencies. Breaches of trust may eventually lead to significant evolution of the international financial system and pave the way for a new system for managing national reserves. Safety will become a priority, so countries will seek to ensure the utmost control over them.

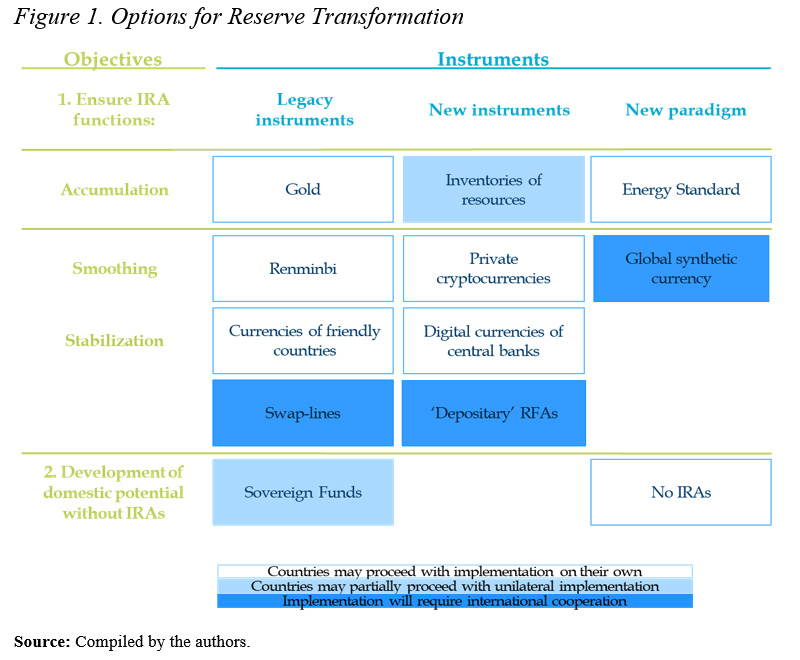

So far, there is no single straightforward solution or instrument to replace traditional currencies and guarantee the safety of assets. Countries can mitigate reserve loss risks through the maximum diversification of accumulation instruments, the fragmentation of reserve functions among instruments, and multi-operator modes of reserve management. The new reserve management system could end up bringing about increased volatility, complexity in management, and higher costs.

The authors identified 12 available options in total (Figure 1), which can be divided into groups according to their characteristics.

This is the widest set of possibilities, but not all of them will necessarily be put into practice. The specific set of tools can be determined by the country depending on its objectives.

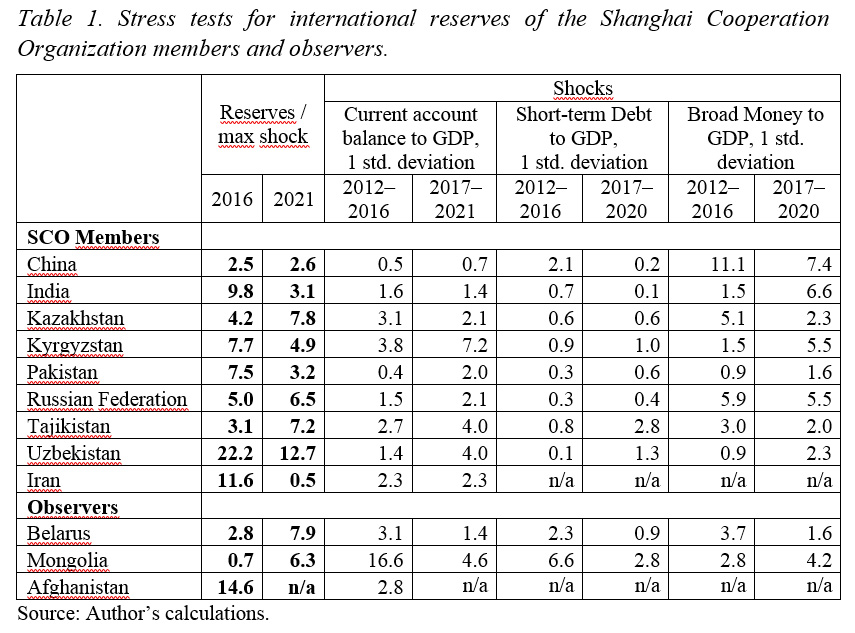

The SCO members and observers may be the first to take steps toward reserve diversification and the introduction of new instruments for their accumulation to develop collective self-sufficiency and strengthen self-defense against global financial and geopolitical turmoil. The SCO consists of nine member states and three observers from Eurasia, which owned approximately $4.8 trillion in their IR in late 2021. The calculations above prove that reserves are not only sufficient, but their amount exceeds potential shocks multiple times. In 2021, they could absorb from two to twelve potential shocks (Table 1).

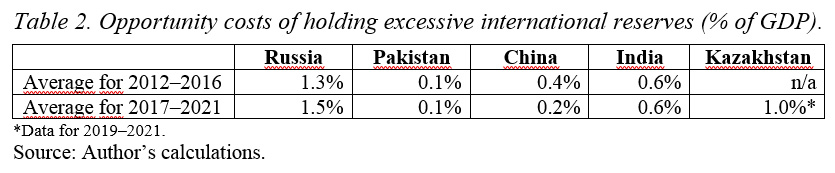

Opportunity costs of holding excessive reserves vary across the countries. Lower middle-income countries acquire significant concessional debt financing, while upper middle-income countries issue debt under general conditions. We believe that China, India, Kazakhstan, and Russia incur consistent direct losses ranging from 0.2 to 1.5% of GDP as their government bonds’ long-term interest rates exceed corresponding U.S. Treasury bond interest rates (Table 2).

The management of IR is of particular concern to the SCO members, as they accumulated significant foreign currency reserves, but three members have already suffered from their freezing. Consequently, it seems plausible for the members of the SCO to expand bilateral currency swaps in the future, promote local currencies in trade and development finance, develop alternative payment and settlement systems, and eventually take action on reducing the U.S. dollar in their reserves.

Overall, the proposed transformation of the reserve management system is likely to advance gradually throughout the 2020s.

The full text of the research paper is available here.