The Eurasian Development Bank (EDB) published its Macroeconomic Forecast with projections for the economic development of its member states for 2021 and the medium term.

The Macroeconomic Forecast states that, at the beginning of this year, the global economy started to steadily recover. The Global PMI Composite Output Index remains above the 50-point threshold and amounted to 53.2 p.p. in February 2021. The Bank’s analysts note that recovery will be proceeding at an uneven pace, with manufacturing remaining the driver, while services continuing to struggle due to persisting constraints.

The EDB expects the global economy to be growing faster in 2021, as the pandemic recedes amid mass vaccinations, and major world economies preserve their current monetary and fiscal stances. The EDB projects the Eurozone’s GDP to grow by 4.3% in 2021, the U.S.’s by 5.5%, and China’s by 8.5%. The average Urals oil price in 2021 is expected to be around US $55 per barrel, which is a comfortable level for the EDB’s region of operations.

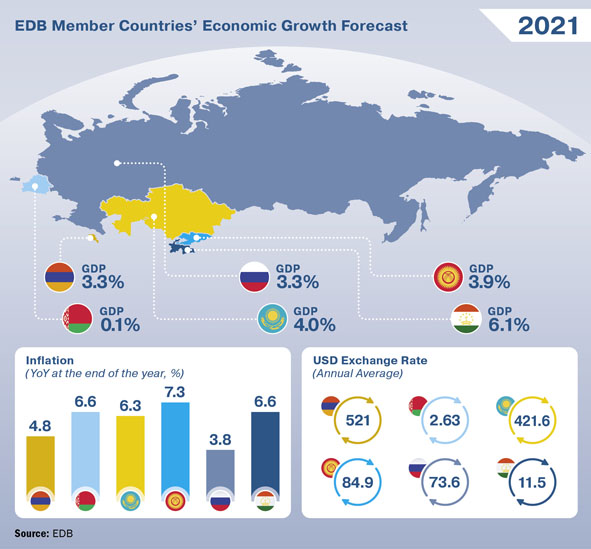

The year 2021 will become a period of strong economic recovery for EDB member states. The Bank projects the aggregated GDP growth rate of its member countries at 3.3%, after a 3% decline in 2020. The easing of social distancing measures and improvement of external economic conditions will be the key drivers of stronger consumer and investment demand. Most of the region’s economies will recover to pre-crisis levels by the end of 2021 and 2022.

The EDB expects its member countries’ currencies to stabilise against the U.S. dollar in 2021. At the beginning of this year, currencies of countries in the EDB region of operations remain relatively stable vs. the US dollar. The national currencies are supported by rising oil prices. At the same time, the Russian rouble continues to be affected by geopolitical risks, which limits the room for its strengthening.

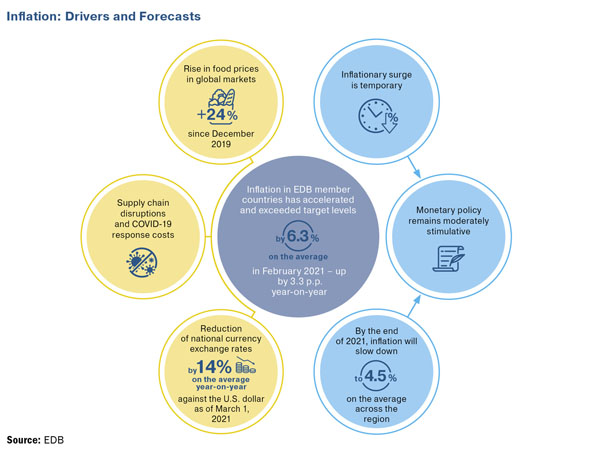

The Macroeconomic Forecast notes that the significant acceleration of inflation in the Bank’s member countries will be temporary and inflation will slow down in the second half of 2021. The main reason for the rise in consumer prices was a substantial global increase in food prices. Under the influence of this factor, inflation in the Bank’s region of operations remained high at the start of the year, averaging 6.3% year-on-year in February 2021. Pandemic-driven supply chain disruptions and COVID-19 response costs have exerted additional pressure on prices. The impact of all these factors on consumer prices will be gradually diminishing over 2021. Combined with stabilisation of the national currency exchange rates, this would help inflation in the region to fall to an average of 4.5% year-on-year by the end of 2021.

“Since the middle of 2020, we have seen a strong global trend in asset inflation,” says Evgeny Vinokurov, the EDB and EFSD Chief Economist. “By the end of February 2021, prices for all key commodity groups exceeded their pre-crisis levels. Food prices are now at its highest since 2013 and industrial metals have not been this expensive since 2011. Having started with metals and food, asset inflation subsequently spread to energy products. Since the beginning of this year, oil price has risen by more than 20% reaching pre-crisis levels. The strong rise in commodity prices is largely due to temporary factors. These include supply disruptions, pandemic-provoked disruptions to production chains, and the rapid recovery of the Chinese economy. Over time, the upward pressure of these factors on commodity prices will be diminishing and their growth will be slowing down. This is the development considered in the EDB’s base case scenario. But above all, asset inflation results from the ultra-soft monetary policies of the world’s major central banks, and the impact of this factor will be quite long-lasting.”

For the Eurasian region, which supplies raw materials to the global market, the rise in prices for metals and energy is generally positive. Export earnings are on the rise, government revenues are growing, and economic sentiment is improving. These positive effects are primarily observed in Russia and Kazakhstan. Thus, if Urals oil prices remain close to US $70 per barrel in the second to fourth quarters of 2021 (more than 20% above the EDB’s base case projection), the Russian economy could grow by 3.7% in 2021, a 0.4 p.p. increase compared to the base case. Kazakhstan’s GDP growth in the optimistic scenario could reach 4.5% in 2021, which is 0.5 p.p. above the base case forecast. Thanks to close economic and financial integration ties, positive effects will spread to other EDB member countries.

EDB analysts also believe that the economies in the Bank’s region of operations will recover, even with the lingering effects of the pandemic, but at a slower pace. The Bank assessed a risky scenario, assuming a slow global economic recovery and falling energy prices. In 2021, Russia’s GDP growth will reach 1.9% in the risky scenario, 1.4 p.p. below the base case forecast. Kazakhstan’s economy in the risky scenario will grow by 1.8 p.p. less than the base case forecast of 2.2%.

You can also view the Macroeconomic Forecast on the EDB website.

Other reports and publications by the EDB and the EFSD are available in the Research section on the Bank’s website and the Research and Publications section on the Fund’s website.