Vinokurov E., Levenkov A., Vasilyev G. (2020) Global Financial Safety Net in Eurasia: Accessibility of Macroeconomic Stabilization Financing in Armenia, Belarus, Kyrgyzstan, and Tajikistan. ЕFSD Working Paper 2020/2, June.

In the working paper, we attempted to expand the traditional scope of the Global Financial Safety Net (international reserves, swap arrangements, regional financing arrangements, and the IMF) with multilateral development banks and bilateral financial support.

Between 2009 and 2019, Armenia, Belarus, Kyrgyzstan, and Tajikistan used a wide range of stabilization financing instruments and sources. The funds disbursed from all the sources in 2009–2019 totalled at least $16 bln. The flow of these resources varied by country and year. Along with the massive financial support from the IMF, Armenia also received significant financing from the EFSD, MDBs, and Russia. Kyrgyzstan has primarily bilateral financial assistance from Russia and IMF financing for stabilization purposes. IMF, EFSD, and MDBs were the three most significant sources in Tajikistan. In Belarus, IMF, Russian bilateral assistance, and EFSD were the most significant sources of stabilization financing.

The swap arrangements in the countries under consideration were used primarily to service foreign trade turnover and did not act as stabilization source as it is usually described in the GFSN-related debates.

The paper traces clear cyclicality of stabilization financing - 2009-10 и 2015-16, which represents the immediate year of a crisis and the year following that.

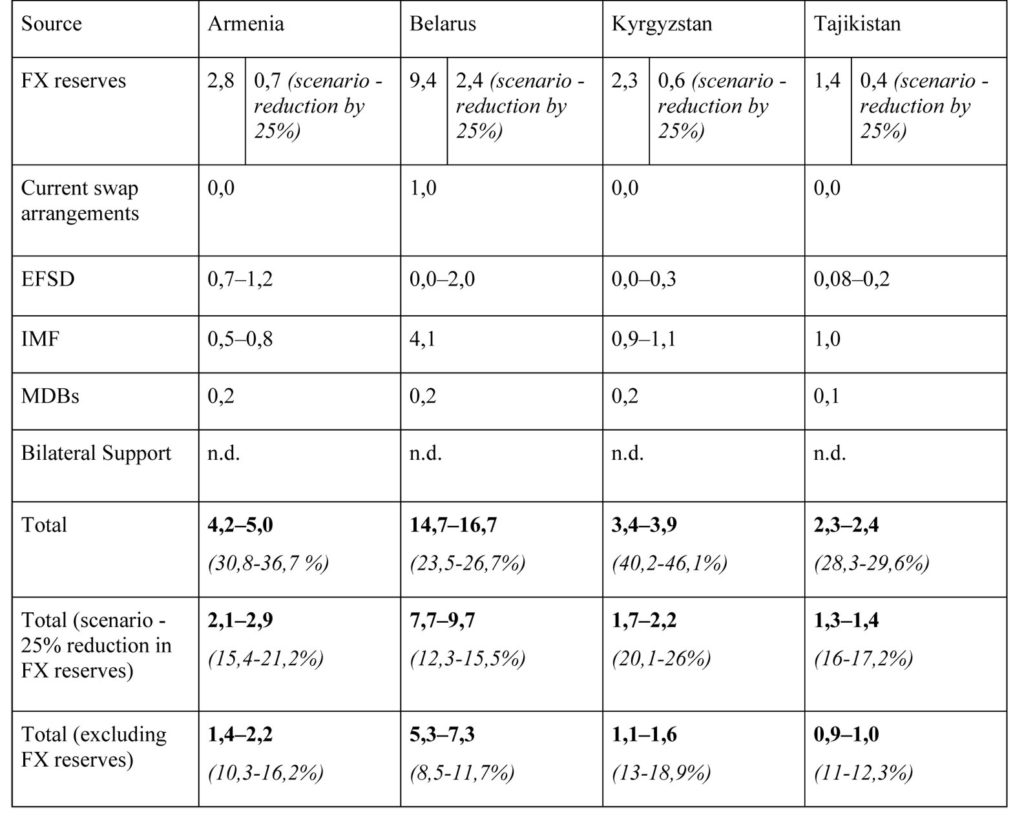

The working paper estimates the availability of stabilization financing for Armenia, Belarus, the Kyrgyz Republic, and Tajikistan based on three approaches (see Table). The first approach summarizes all available sources of stabilization financing. However, two other approaches – with national reserves decreasing by 25% in absolute terms and not taking into account the national reserves at all – are more practical for purposes of analysis (since massive depletion of the national reserves is an extreme scenario which would result in a balance of payments’ crisis). The calculations provided in the table below do not comprise data for bilateral support, so the final total represents a conservative estimate.

Table. Analytical Assessment of Indicative Accessibility of Stabilization Financing Sources by Country, $ bln (percentage of GDP in brackets), as of end-2019

When calculating accessibility, the authors take in to account qualitative aspects, such as donor coordination, the degree of conditionality of financing, varying terms and other peculiarities of the financing instruments, as well as the limited public access to information, in particular, on bilateral support and the use of swap arrangements.

The COVID-induced crisis will evidently lead to the next wave of anti-crisis financing. First, in 2020, it will manifest itself in the large-scale emergency lending (the ‘fire-fighting’) aiming at supporting national budgets and balance of payments, maintaining social spending, and ramping up the health care. In 2021, it is to expect that a wave of stabilization programs with the more long-term and structural effects would follow.

You can also view the report on the EFSD official website.