EDB Macroeconomic Outlook 2023–2025

The Eurasian Development Bank has published its Macroeconomic Outlook for 2023–2025. This analysis summarises economic developments in the Bank’s member states in early 2023 and provides key macroeconomic projections for the region’s countries until the end of the year and for 2024–2025.

EDB analysts have continued to share their perspectives on the three major trends observed in the global economy and their impact on Eurasia. The first trend is a slowdown in inflation, which is still expected to remain higher than in the previous decade. The second one is the conclusion of monetary tightening cycles in developed countries. The third is weaker global economic growth.

The external environment for Eurasian economies in 2023 will be characterised by high inflation in developed countries and subdued demand for the region’s exports. Evgeny Vinokurov, Chief Economist at the EDB, highlights a significant slowdown in the global economy: “Higher inflation and sharply increased interest rates will hinder economic growth in major economies. We estimate US GDP growth at 0.4% in 2023. We also acknowledge the possibility of a recession in some quarters of 2023 and 2024, with a meaningful recovery growth of 2.8% expected only in 2025. In the eurozone, the recovery will be even slower, projected at 0.3% in 2023 and 1.9% in 2025. Meanwhile, in China, GDP growth is expected to accelerate to 5.6% in 2023 as strict quarantine policies are abandoned, but there are preconditions for a medium-term slowdown in the Chinese economy. With the US election cycle, turbulence in the financial sector and increased recession risks will push the Fed to cut rates as early as Q3 2023. The ECB will also complete its cycle of rate hikes by mid-year and is expected to reverse its trajectory by the end of 2023 or the beginning of 2024. We believe that the world will not revert to the ultra-low inflation and rates witnessed in the 2010s and forecast the average inflation rate for 2023–2025 at 3.6% year-on-year in the US and 3.7% year-on-year in the eurozone.”

EDB economies are expected to exhibit high resilience to the adverse external economic environment in the medium term. The outlook for 2023 has been revised positively for all the Bank’s member states. The main factors driving this revision include the strong performance observed at the beginning of this year amid the relatively swift adaptation of the economies to changes in the operating environment in 2022 and the implementation of fiscal support measures in certain countries. EDB analysts project the region’s GDP to grow by 1.5% by 2023.

Outlook for the main macroeconomic indicators of EDB member states

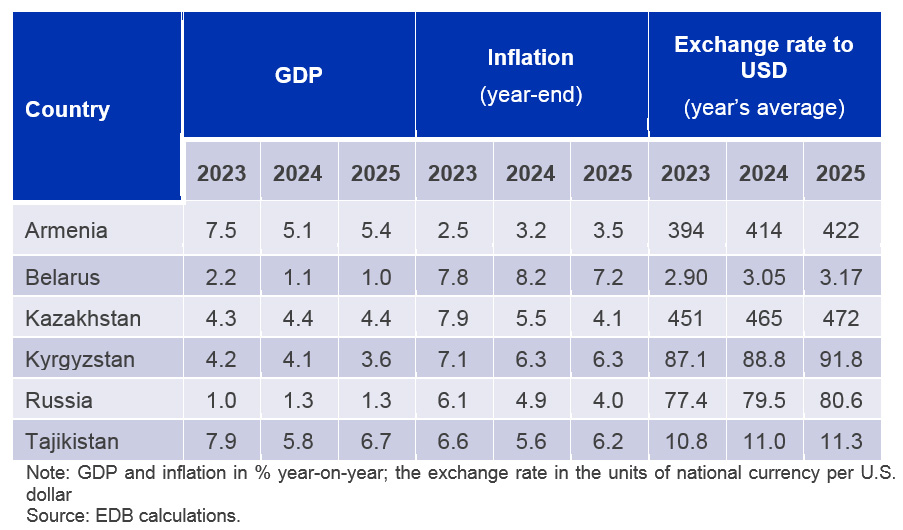

The economies of Russia and Belarus are expected to resume growth in the first half of 2023. By the end of 2023, Russia’s GDP is projected to increase by 1%, with continued growth at an annual rate of approximately 1.3% in 2024–2025. The recovery of demand in Russia and the partial restructuring of supply chains will contribute to Belarus’s economic growth at 2.2% in 2023, stabilising at around 1% thereafter. In the medium term, business activity in these countries will continue to face challenges such as heightened uncertainty, difficulties in supplying investment and intermediate goods, and limited access to advanced technologies.

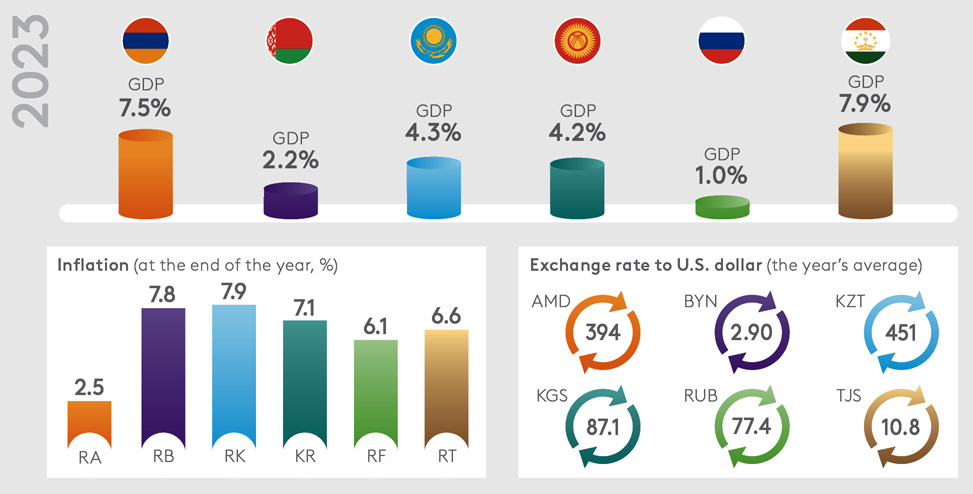

Kazakhstan’s economic growth could reach 4.3% in 2023 and 4.4% in 2024-2025. The government’s initiatives aimed at diversifying the economy, strengthening investment potential, and expanding production capacity will support economic activity. Additionally, strong domestic demand and increased mutual trade will ensure high growth rates by the end of 2023 in other EDB member states: Armenia’s GDP is projected to increase by 7.5%, Kyrgyzstan’s by 4.2%, and Tajikistan’s by 7.9%.

EDB analysts anticipate that aggregate inflation in the Bank’s region will decline to 6.4% by the end of 2023, compared to 12.4% in 2022. This slowdown in inflation can be attributed to the adjustment of the economies and a recovery from the shock experienced in early 2022, when there was a sharp increase in devaluation and inflation expectations. Inflation is projected to be at 2.5% in Armenia, 7.8% in Belarus, 7.9% in Kazakhstan, 7.1% in Kyrgyzstan, 6.1% in Russia, and 6.6% in Tajikistan. In most of the region, inflation is expected to approach the target values in 2024–2025.

The projected slowdown in inflation paves the way for central/national banks in most countries to reduce their key rates in the medium term. The National Bank of Kazakhstan may initiate a gradual reduction of the base rate starting in the second half of 2023, and there is a potential for its reduction to 15% by the end of the year, compared to 16.75% at the end of May. If inflationary pressures from the external sector ease, the rate could further decrease to 11–12% by the end of 2024. EDB analysts expect the Bank of Russia’s key interest rate to remain at 7.5% per annum in 2023 and gradually decline to 6–6.5% in 2024–2025.

The baseline scenario does not anticipate any sustained deviation of the Russian rouble from its current values. The projected average RUB/USD exchange rate for 2023 is 77.4, with an expectation of reaching 79 by the end of the year. The weakening of the rouble at the end of 2022 and the beginning of 2023 has eliminated its overvaluation that occurred in 2022. Going forward, exchange rate developments are expected to be primarily influenced by the balance of trade, where rising imports due to recovering domestic demand will be counterbalanced by growing export earnings as the discount on Russian oil diminishes. The exchange rate of Kazakhstan’s tenge is forecast to remain stable for the rest of 2023. The high base rate will continue to support the attractiveness of Kazakhstan’s financial assets. As the rate decreases, a reversal in the dynamics of the tenge’s exchange rate can be expected. The KZT/USD exchange rate is projected to average 451 in 2023 and 465 in 2024.

EDB forecasts. Main macroeconomic indicators of the EDB member states (baseline scenario)

You can also view the EDB Macroeconomic Outlook at the EDB website.