The Eurasian Development Bank has published its Macroeconomic Outlook for 2022–2024. The analysis summarises economic developments in the Bank’s member states in 2022 and provides key macroeconomic projections for the region’s countries for 2022–2024.

EDB analysts note that the global economy has entered a period of sustained turbulence. The hopes for sustained post-pandemic economic growth are all but nullified. Energy, food and fertiliser prices have reached multi-year highs, exacerbating last year’s inflation problem. The major central banks have had to react to the massive inflation and have already started to tighten monetary policies. The global economy is once again witnessing disruptions in production and logistics chains, and weakening consumer and investment activity. This combination of supply and demand shocks suggests a slowdown in the post-pandemic recovery and a fairly substantial likelihood of a recession in the world’s major economies in 2022–2023.

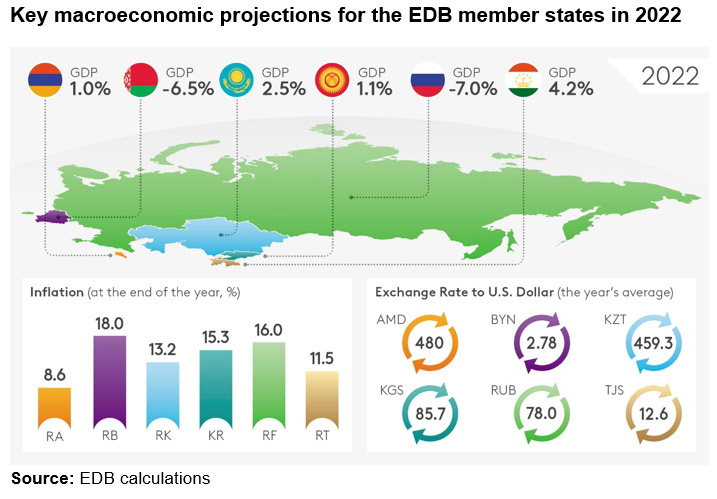

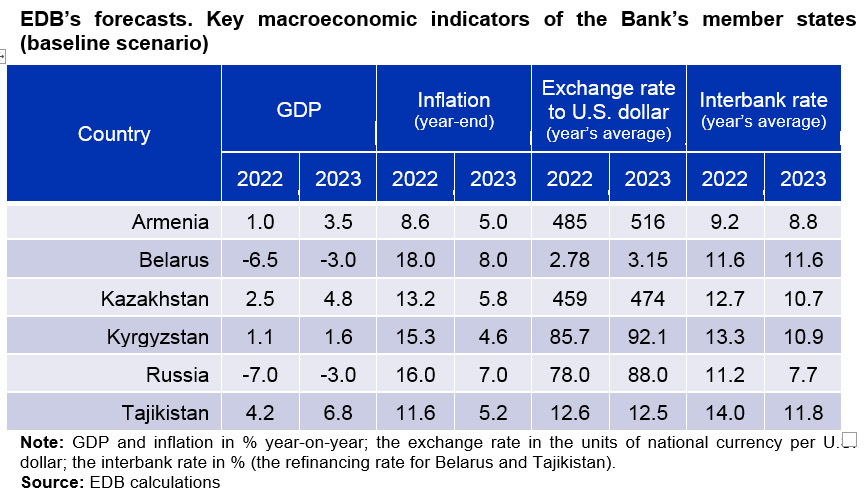

EDB analysts forecast diverging dynamics for the region’s economies in 2022. The baseline scenario projects Russia’s GDP to contract by 7.0% in 2022. A significant decline of 6.5% is also projected for Belarus. All this will result from disruptions in production and logistics chains, increased uncertainty, and sanctions. The growth of the other member economies will slow down due to their close economic ties with Russia and slower growth of the global economy. By the end of 2022, GDP growth in Armenia is projected at 1.0%, Kazakhstan at 2.5%, Kyrgyzstan at 1.1%, and Tajikistan at 4.2%.

It will take longer for the EDB region’s aggregate growth rates to return to positive values than in previous crisis periods. While GDP contractions in 2009, 2015, and 2020 in most of the region’s countries were followed by growth the following year, the economic slowdown in 2022 is likely to be followed by growth in Russia and Belarus in 2024 only. However, the other EDB member countries are expected to see an acceleration in growth rates as early as 2023. According to the baseline projections, Kazakhstan’s economy will grow by 4.8% in 2023, driven by increased consumer and investment activity and government programmes aimed at improving household incomes and promoting business development. GDP growth in Kyrgyzstan and Armenia will be 1.6% and 3.5%, respectively, as a result of exporters and migrant workers’ reorientation to new markets.

EDB analysts note higher inflation in the Bank’s region of operations in March and April 2022 and believe that it will remain elevated in 2023. By the end of this year, consumer price growth will accelerate to a maximum of 16% and 18% in Russia and Belarus, respectively. The main factors are supply chain disruptions, greater volatility of national currencies, higher devaluation and inflationary expectations, and rising commodity prices. In the countries that are not directly affected by the restrictions, the inflation surge by the end of 2022 will be smaller: 8.6% in Armenia, 13.2% in Kazakhstan, 15.3% in the Kyrgyz Republic, and 11.5% in Tajikistan.

EDB analysts believe that monetary conditions in 2022 will be determined by a balance of fighting inflation and supporting economic activity. By the end of the year, the key rates could fall to around 9% in Russia (from 11% in May) and 12% in Kazakhstan (from the current 14%). As inflation slows down, the key rates in Russia and Kazakhstan are expected to decrease actively in 2023 and return to single-digit levels.

The risk of inflation in developed countries accelerating above 10% remains significant. Should hydrocarbon and food-related risks materialise, this could cause further increases in global inflation and trigger a global recession in early 2023. The economic downturn in such an adverse scenario would be small, but the recovery could be long and difficult.

The Macroeconomic Outlook is available on the EDB website.