The Eurasian Development Bank (EDB) has released its Macroeconomic Outlook for the Bank’s six member states. The analytical material analyzes the economic developments in its member countries for 2024 and provided forecasts for their key macroeconomic indicators through the end of 2024 and into 2025–26.

EDB analysts estimate that the global economy will continue to grow at around 3% in 2024, driven largely by emerging economies. The rate of decline in inflation in developed nations is slowing due to labour market imbalances caused by labour shortages and rising costs associated with global economic fragmentation. This is expected to result in a prolonged period of high interest rates in the US and the euro area, affecting their economic growth. The US GDP is projected to grow by 1.9% in 2024, down from 2.5% in 2023, due to lower consumer activity. Economic growth in the euro area is expected to remain sluggish, hovering around the previous year’s rate of around 0.5%. In contrast, China’s economy is anticipated to exceed its 5% growth target again, supported by government incentives. EDB analysts do not foresee a broad-based increase in commodity prices globally.

For most EDB member countries, the outlook has been upgraded due to strong early-year performance and continued robust utilisation of domestic growth sources. Stimulative fiscal policies and structural transformations are fostering an environment conducive to investment and consumer activity. EDB analysts forecast a 3.4% growth in the region’s GDP by the end of 2024.

Key macroeconomic forecasts for the EDB member states in 2024

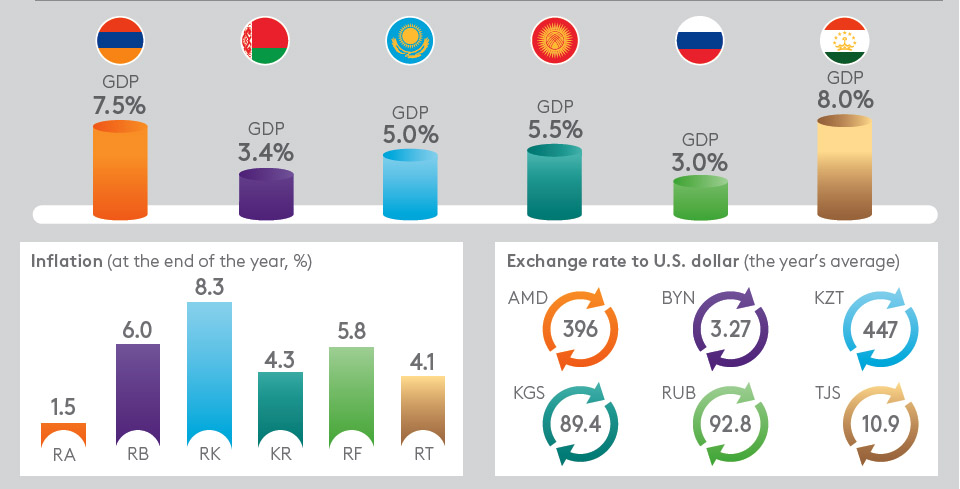

In Armenia, Kyrgyzstan and Tajikistan, high growth rates in early 2024, driven by strong domestic demand and increased exports of basic metals, have led to upgraded GDP growth projections for 2024: 7.5% for Armenia, 5.5% for Kyrgyzstan and 8.0% for Tajikistan.

Kazakhstan’s economy is expected to maintain a high GDP growth rate of around 5% in 2024. Government efforts to diversify the economy are anticipated to catalyse and sustain a steady GDP growth rate in the medium term.

Russia’s GDP growth forecast for 2024 has been improved to 3.0%. EDB analysts note that domestic demand has expanded further, driven by high household incomes and fiscal stimuli. However, consumer activity is expected to gradually decline over the forecast period due to tight monetary policy.

Belarus’s GDP growth forecast for 2024 has been upgraded to 3.4%, supported by continued strong growth in demand from Russia and wage increases.

EDB researchers expect the inflationary trend across the Bank’s region to slow further, with the aggregate inflation rate decreasing to 5.8% by the end of 2024 from 7.2% in 2023. Inflation remains heterogeneous across the region: Armenia continues to experience deflation, while inflation in Kyrgyzstan and Tajikistan may drop below target levels.

Conversely, Russia and Kazakhstan continue to face increased inflationary pressures. Bank analysts project that inflation rates will gradually approach targets in 2024: 1.5% in Armenia, 6% in Belarus, 8.3% in Kazakhstan, 4.3% in Kyrgyzstan, 5.8% in Russia and 4.1% in Tajikistan.

Despite declining inflation rates, persistent inflation risks in the EDB’s larger economies are expected to lead to the regulators’ cautious approach to monetary easing in 2024. EDB analysts anticipate that Kazakhstan’s base rate will remain above 13% by the end of 2024. The Bank of Russia is forecast to begin a cycle of rate cuts this year, with the inflation rate expected to decline to 15% per annum by year-end.

The full version of the report EDB Macroeconomic Outlook 2024–2026 is available at the EDB website.